Rising interest rates are a drag on returns.

In May 2015 I created an income portfolio designed for TFSAs for readers of my Income Investor newsletter. The goal was to generate cash flow in the 5 per cent range. This makes it especially useful for older people who want to receive tax-free income. You can withdraw the dividends/distributions earned each year without paying any tax, while leaving the principle intact.

However, this type of portfolio comes with some risk. For starters, it is entirely invested in stocks, which makes it more vulnerable than a balanced portfolio that includes bond holdings. For another, dividend-paying stocks tend to come under pressure as rates rise, as we’ll see when we review the numbers from the latest six-month period.

At the time I launched this portfolio, the maximum cumulative lifetime contribution was $41,000, so that was the initial starting value.

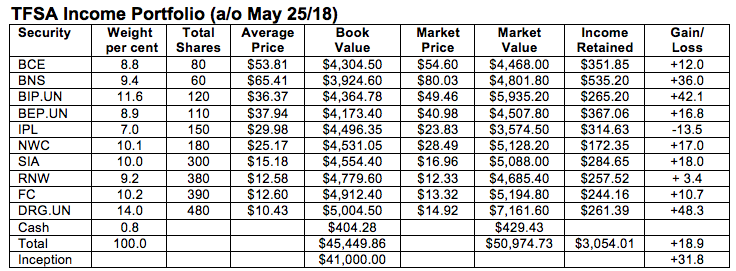

I selected 10 securities from the Income Investor Recommended List. All are traded on the TSX, so currency exchange is not a factor, except for the distributions from the limited partnerships, which are in U.S. dollars. I gave each security an initial weighting of approximately 10 per cent for diversification and balance. Here are the components of the portfolio with a brief report on how they have performed since the last update in November. Prices are as of the close of trading on May 25.

BCE Inc. (TSX, NYSE: BNS). BCE was one of the stocks hit by rising rates. The shares have dropped by $7.12 since November, a decline of about 15 per cent. This was despite an increase in the dividend of 5.2 per cent earlier this year, bringing the quarterly payout to $0.755 ($3.02 per year). As a result of the price decline and the dividend increase, the stock now yields a very attractive 5.5 per cent.

Bank of Nova Scotia (TSE, NYSE: BNS). Banks are supposed to prosper as rates increase, but we have not seen that in BNS shares, which are down $4.56 since November. As with BCE, we had a dividend increase at the start of the year with the quarterly payout rising 3.8 per cent to $0.82 per share ($3.28 a year). As a result, the yield jumped to 4.1 per cent from 3.8 per cent at the time of the last review.

Brookfield Infrastructure Limited Partnership (TSX: BIP.UN, NYSE: BIP). This Bermuda-based limited partnership is a spinoff company from Brookfield Asset Management, which owns a majority stake. It invests in infrastructure projects in North and South America, Europe, and Australia. Like other interest-sensitive stocks, this one is down from our November review. The partnership increased its distribution by 8 per cent in February, to US$0.47 per quarter (US$1.88 per year). That and the price drop pushed the yield to 4.9 per cent.

Brookfield Renewable Partners (TSX: BEP.UN, NYSE: BEP). This is another Brookfield spinoff, but with a focus on renewable energy, mainly hydro but also some wind projects. The units are down $2.02 from the time of our last review. We received two distributions totaling US$0.9575, as the partnership implemented a 4.8 per cent increase in February. The units yield 6.2 per cent at the current price.

Inter Pipeline (TSX: IPL, OTC: IPPLF). This stock has been a disappointment. It was off another $2.51 in the latest period and is down 13.5 per cent overall since the portfolio’s inception. We will replace it with a similar but more dynamic company (see below).

North West Company (TSX: NWC, OTC: NWTUF). The shares declined by $3.51 in the latest period. The quarterly dividend is $0.32 per share, and we received two payments. The current yield is 4.5 per cent.

Sienna Senior Living Inc. (TSX: SIA, OTC: LWSCF). Sienna’s share price was down $1.33 during the latest review period. However, the monthly dividends of $0.075 per share continued to roll in. The current yield is 5.3 per cent.

TransAlta Renewables Inc. (TSX: RNW, OTC: TRSWF). This stock took another hit in during the past six months, dropping $0.87 in value. The monthly payment is $0.0783 per share ($0.9396 per year). The price retreat pushed the yield to 7.6 per cent.

Firm Capital MIC (TSX: FC). Despite rising rates, the share price of this mortgage investment corporation increased by $0.51 in the latest period. The monthly payment remains at $0.078 ($0.936 per year) to yield 7 per cent.

Dream Global REIT (TSX: DRG.UN). This international REIT invests in office, industrial, and mixed-use properties in Europe. We added it to the portfolio a year ago, and so far, it has paid off well. The share price was up $3.27 (28 per cent) in the latest period, and the units pay $0.0666 per month, or about $0.80 per year. The yield is 5.4 per cent at the current price. This is the best-performing security in the portfolio at this time.

We received interest of $25.15 during the latest period from our EQ Bank savings account.

Here is how the portfolio looked at the close of trading on May 25.

Comments: The value of the portfolio (market price plus retained earnings) declined by $455.54, or 0.8 per cent, during the latest six-month period. It could have been much worse considering the overall downtrend in interest-sensitive stocks, but gains in Firm Capital, and especially Dream Global REIT, plus strong distributions helped to stem the loss.

Despite the recent loss, since the portfolio was launched three years ago, it has posted a gain of 31.5 per cent. On an annualized basis, that works out to 9.63 per cent, which is still very respectable for a portfolio of this type.

Cash flow during the latest period was $1,401.80, for a six-month yield of 2.57 per cent based on the portfolio value last November. In terms of the original $41,000 investment, the six-month yield was 3.42 per cent, so we are well ahead of our 5 per cent annual cash flow target.

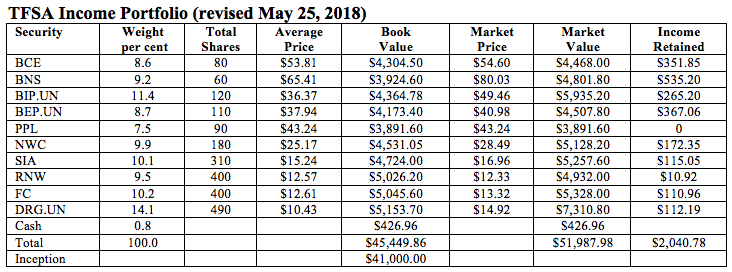

Changes: We will replace Inter Pipeline with shares of Pembina Pipeline (TSX: PPL). Yes, we’re still in the pipeline business, which means the stock is interest-sensitive, but it has held up much better in the current climate than Inter.

The total value of our Inter Pipeline position, including retained dividends, is $3,889.13. Pembina is trading at $43.24 and has a yield of 5.2 per cent. We will buy 90 shares for $3,891.60. We will take the difference of $2.47 from cash.

We will also make some additional small purchases as follows:

SIA – We will add 10 shares at a cost of $169.60. That will bring our position to 310 shares and reduce our retained earnings to $115.05.

RNW – We will buy another 20 shares for $246.60, leaving cash of $79. We now own 400 shares with a cash balance of $10.92.

FC – We will add 10 shares at a cost of $133.20 to a new total of 400. Our cash balance will be reduced to $110.96.

DRG.UN – We will buy another 10 shares for $149.20, bringing our total to 490. We will have $112.19 left in cash.

Readers are reminded not to do small trades unless you have a fee-based account. Use a dividend reinvestment plans when available.

We will keep our cash of $2,467.74 in the EQ Bank savings account, which still pays 2.3 per cent.

Here is the revised portfolio. I will look at it again in November.

Gordon Pape is Editor and Publisher of the Internet Wealth Builder and Income Investor newsletters. For more information and details on how to subscribe, go to www.buildingwealth.ca.

'%3E %3Cg id='Group'%3E %3Cpath id='Vector_2' d='M12.4876 13.8996V13.4213H0.743091V15.2149H9.18805L9.22196 15.2685C9.19653 15.2272 3.24373 25.2836 0.74521 29.5469C0.420975 30.1015 0.0797856 30.7158 0.0797856 30.7158C0.0713089 30.7323 0.0585938 30.755 0.0585938 30.755H12.1401V28.9614H3.67181L3.6379 28.9078C3.37512 29.1222 12.4876 13.8996 12.4876 13.8996ZM36.1229 22.115C36.1229 26.4896 33.7537 29.18 31.1683 29.18C28.5829 29.18 26.1861 26.4896 26.1861 22.115C26.1861 17.7403 28.5553 15.0231 31.1683 15.0231C33.7812 15.0231 36.1229 17.7403 36.1229 22.115ZM22.0155 22.115C22.0155 26.4896 19.6462 29.18 17.0587 29.18C14.4712 29.18 12.0765 26.4896 12.0765 22.115C12.0765 17.7403 14.4458 15.0231 17.0587 15.0231C19.6717 15.0231 22.0155 17.7403 22.0155 22.115ZM38.223 22.0613C38.223 16.7095 35.0443 13.1492 31.1661 13.1492C27.288 13.1492 24.3402 16.4312 24.0987 21.4326C23.8592 16.4333 20.7842 13.1492 17.0587 13.1492C13.3332 13.1492 9.97427 16.7074 9.97427 22.0613C9.97427 27.4153 13.1785 31.0003 17.0587 31.0003C20.9389 31.0003 23.8592 27.7183 24.0987 22.6922C24.3402 27.7162 27.4406 31.0003 31.1661 31.0003C34.8917 31.0003 38.223 27.4421 38.223 22.0613ZM51.3747 30.755H53.5257L52.3178 13.4213H50.1668L45.797 27.3328L41.4273 13.4213H39.2763L38.0662 30.755H40.2172L41.0352 19.0247L44.7205 30.755H46.8714L50.5567 19.0247L51.3747 30.755ZM53.9453 30.755H62.3797V28.9614H56.0963V22.9293H60.964V21.1357H56.0963V15.2128H61.8859V13.4192H53.9453V30.7529V30.755ZM69.3624 18.2021C69.3624 20.1029 68.1333 21.1625 66.7367 21.1625H64.893V15.2128H66.7092C68.1333 15.2128 69.3624 16.3261 69.3624 18.2021ZM71.5134 18.1753C71.5134 15.2128 69.3348 13.4213 67.0164 13.4213H62.7993V30.755H64.893V22.9313H66.7092L71.5112 30.755H73.997L68.8601 22.4695C70.369 21.8717 71.5134 20.3502 71.5134 18.1773' fill='%23231F20'/%3E %3C/g%3E %3C/g%3E %3C/g%3E %3Cg id='Group_2'%3E %3Cpath id='Vector_3' d='M9.67285 8.56629V3.50513H12.6249V4.11535H10.5947V5.71719H12.2943V6.32742H10.5947V7.954H12.9046V8.56423H9.67285V8.56629Z' fill='%23231F20'/%3E %3Cpath id='Vector_4' d='M17.6819 8.6137H17.2581L15.1855 3.50513H16.1392L17.0822 5.86975C17.2178 6.20991 17.362 6.63872 17.4976 7.05103H17.5188C17.6544 6.64696 17.7879 6.2264 17.9341 5.86975L18.8666 3.50513H19.7482L17.6862 8.6137H17.6819Z' fill='%23231F20'/%3E %3Cpath id='Vector_5' d='M22.4072 8.56629V3.50513H25.3593V4.11535H23.3291V5.71719H25.0287V6.32742H23.3291V7.954H25.639V8.56423H22.4072V8.56629Z' fill='%23231F20'/%3E %3Cpath id='Vector_6' d='M31.6164 8.56629L29.9698 6.32123H29.2959V8.56629H28.374V3.50513H30.0948C30.9552 3.50513 31.805 4.01227 31.805 4.90906C31.805 5.54402 31.3896 5.97283 30.8725 6.16249L32.6654 8.56629H31.6185H31.6164ZM29.9592 4.10711H29.2959V5.71719H29.9592C30.436 5.71719 30.8704 5.43888 30.8704 4.90906C30.8704 4.37923 30.436 4.10711 29.9592 4.10711Z' fill='%23231F20'/%3E %3Cpath id='Vector_7' d='M37.5849 6.27382V8.56629H36.6737V6.28206L34.6943 3.50513H35.667L36.6503 4.90081C36.8156 5.13789 37.0021 5.38528 37.1378 5.59968H37.159C37.3031 5.39353 37.5001 5.11522 37.657 4.90081L38.6403 3.50513H39.5621L37.5828 6.27382H37.5849Z' fill='%23231F20'/%3E %3Cpath id='Vector_8' d='M44.3084 4.11535V8.56629H43.376V4.11535H41.7188V3.50513H45.9656V4.11535H44.3084Z' fill='%23231F20'/%3E %3Cpath id='Vector_9' d='M52.0484 8.56629V6.32948H49.499V8.56629H48.5771V3.50513H49.499V5.71926H52.0484V3.50513H52.9808V8.56629H52.0484Z' fill='%23231F20'/%3E %3Cpath id='Vector_10' d='M56.2129 8.56629V3.50513H57.1453V8.56629H56.2129Z' fill='%23231F20'/%3E %3Cpath id='Vector_11' d='M64.7402 8.64463L62.4091 6.17693C62.0467 5.79553 61.6208 5.31106 61.2796 4.91524L61.2584 4.92349C61.2796 5.3523 61.2902 5.7811 61.2902 6.13776V8.56629H60.3789V3.50513H61.0316L63.1868 5.82233C63.4878 6.14806 63.9222 6.63872 64.2337 7.00362L64.2549 6.99537C64.2337 6.62223 64.2231 6.17899 64.2231 5.83677V3.50513H65.1344V8.64669H64.7402V8.64463Z' fill='%23231F20'/%3E %3Cpath id='Vector_12' d='M70.9048 8.64416C69.4235 8.64416 68.0566 7.69172 68.0566 6.03421C68.0566 4.37671 69.4659 3.41602 70.8752 3.41602C71.5999 3.41602 72.17 3.57476 72.5324 3.78091L72.3883 4.42412C72.0471 4.21797 71.5491 4.05098 71.0002 4.05098C69.9639 4.05098 68.9912 4.77253 68.9912 6.04246C68.9912 7.31239 69.9448 8.01745 70.9599 8.01745C71.405 8.01745 71.7567 7.93911 71.975 7.7948V6.61352H70.8349V6.03421H72.8354V8.12877C72.3586 8.47718 71.7271 8.64416 70.9091 8.64416H70.9048Z' fill='%23231F20'/%3E %3C/g%3E %3Cpath id='Vector_13' d='M0.0839844 1.00212L73.997 1' stroke='%23231F20' stroke-width='1.25' stroke-miterlimit='10'/%3E %3Cpath id='Vector_14' d='M0.0839844 10.9116H73.997' stroke='%23231F20' stroke-width='1.25' stroke-miterlimit='10'/%3E %3Cpath id='Vector_15' d='M4.91016 4.15649L3.55812 4.13794L5.18777 5.7068L0 5.6532V6.5974L5.20049 6.651L3.61321 8.18068L4.96526 8.19718L7.0018 6.20157L4.91016 4.15649Z' fill='%23D71920'/%3E %3C/g%3E %3C/svg%3E)