Gordon Pape: Advice on How to Overhaul Your RRSP Portfolio

Overhauling your RRSP can be a puzzle. Photo: Pixabay

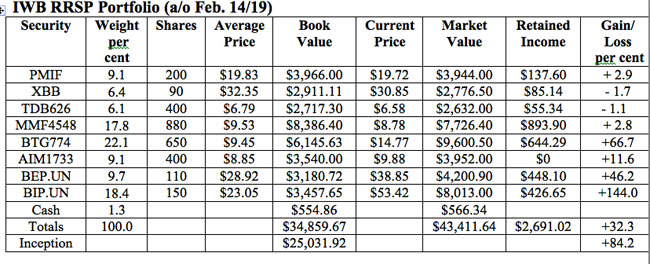

Now that you have (presumably) made your RRSP contribution for this year, the question becomes where should it be invested? For some ideas, let’s take a look at my model RRSP Portfolio. It was set up in February 2012, so this is its seventh anniversary.

The portfolio has two main objectives: to preserve capital and to earn a higher rate of return than you could get from a GIC. The original value was $25,031.92.

About a fifth of the portfolio is in bonds and cash. The balance is in growth-oriented assets that offer exposure to the Canadian, U.S., and international equity markets. The portfolio contains a mix of ETFs, mutual funds, and limited partnerships so readers who wish to replicate it must have a self-directed RRSP with a brokerage firm.

These are the securities currently in the portfolio with some comments on how they have performed since the last review in October. Stock results are as of the afternoon of Feb. 14. Mutual fund results are as of the close on Feb. 13.

PIMCO Monthly Income ETF (TSX: PMIF). This fund invests in a portfolio of global bonds and pays monthly distributions. It was added in February 2018 at $19.83. The unit value dropped over the summer, reflecting rising interest rates. However, the value has recovered by $0.25 since our last review in October plus we received dividends of $0.28 a share for a return of 2.7 per cent over the four months.

iShares Canadian Universe Bond Index ETF (TSX: XBB). This ETF tracks the performance of the total Canadian bond universe including government and corporate issues. Bonds have rebounded recently as the economy slows and central banks have signalled a pause in rate increases. The fund has gained $0.83 since the last review plus we received distributions of $0.296 per unit for an advance of 3.75 per cent in four months.

TD High Yield Bond Fund I units (TDB626). This high-yield bond fund was added in early 2017 in an effort to boost returns from our fixed income holdings. It has been a disappointment and to date we have a net loss of 1.1 per cent.

Manulife Dividend Income Plus Fund Advisor Series (MMF4548). This is an equity fund with a small bond position. About 52 per cent is invested in Canada, 27 per cent in U.S. stocks, with the rest scattered around amongst other countries. The NAV is down $0.93 since the last review but that was offset by distributions of $0.9558 per unit.

Beutel Goodman American Equity Fund D units (BTG774). The unit value is down $0.82 since the last review. However, we received a year-end distribution of just over $0.99 per unit in December so we had a net gain during the period.

Invesco International Companies Fund, A units (AIM1733). This fund had been on a slide but rallied modestly in the latest period to gain 5.2 per cent. It did not pay any distributions.

Brookfield Renewable Energy Partners LP (TSX: BEP.UN, NYSE: BEP). This Bermuda-based limited partnership owns a range of renewable power installations (mainly hydroelectric but also some wind), mostly in North and South America. The share price is up $0.66 since the last review and we received one distribution of US$0.49 per unit.

Brookfield Infrastructure Partners LP (TSX: BIP.UN, NYSE: BIP). This limited partnership invests in infrastructure projects around the world. It has been the best performer in the portfolio and recovered from a temporary slump to gain $1.18 in the latest period. We received one distribution of US$0.49.

Interest. We invested $1,497.05 in an account with EQ Bank, which is paying 2.3 per cent. We received $11.48 for the period.

Here is how the RRSP Portfolio stood as of Feb. 14. Commissions have not been factored in and Canadian and U.S. currencies are treated at par for ease of tracking.

Comments: Our bond holdings did somewhat better in the latest period as market rates slipped as both the Federal Reserve Board and the Bank of Canada indicated a pause in rate hikes.

The overall portfolio registered a modest gain of $874.61 for the period, or 1.9 per cent. In the seven years since this portfolio was launched the average annual gain is 9.1 per cent. That’s in excess of our target, despite the weak returns of the past year.

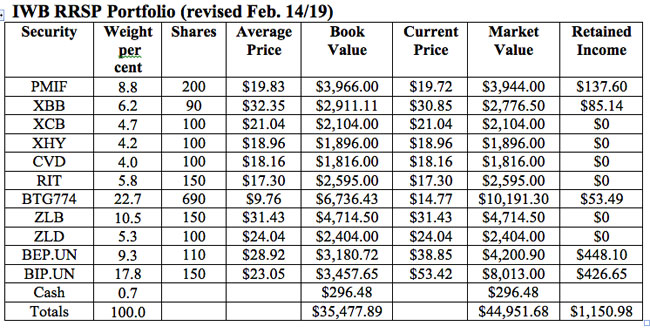

Changes: I’m going to do a major overhaul of this fund. I don’t do this often, but the portfolio has not been performing to my standards for a couple of years so it’s time for some changes. At the same time, this provides an opportunity to reduce the carrying costs of the portfolio by replacing mutual funds with ETFs.

For starters, we will sell three of our mutual fund positions: TD High Yield Bond Fund, Manulife Dividend Income Plus Fund, and Invesco International Companies Fund. This will give us $15,259.64 to reinvest. We will start by diversifying our bond holdings as follows:

iShares Canadian Corporate Bond Index ETF (TSX: XCB). This fund invests exclusively in corporate issues, as opposed to XBB, which covers the entire Canadian bond universe. It generated an average annual gain of 5.2 per cent over the 10 years to Jan. 31 and is ahead 2 per cent this year (to Feb. 14). The MER is 0.44 per cent. Distributions are made monthly and are currently $0.053 per unit. We will buy 100 units at $21.04 for an investment of $2,104.

iShares U.S. High Yield Bond Index ETF (CAD-Hedged) (TSX: XHY). High-yield bond ETFs can be volatile but over the years they have generated good results. This one was launched in January 2010 and has produced an average annual return of 5.65 per cent since inception. It’s coming off weak year but has been doing very well lately with a gain of 5.15 per cent so far in 2019. The MER is 0.67 per cent. Distributions are paid monthly, the most recent being $0.087 per unit. We will buy 100 units at $18.96 for an investment of $1,896.

iShares Convertible Bond Index ETF (TSX: CVD). This fund specializes in bonds that can be converted into common stocks under certain conditions. It has been around since 2011 with an average annual return since inception of 3.5 per cent. So far this year it is up about 2 per cent. Distributions are monthly at $0.07 per unit. The MER is 0.5 per cent. We’ll buy 100 units at $18.16 for a cost of $1,816.

Turning to equities, an RRSP should have some REIT exposure. There are several good choices available, including XRE from iShares. But we’re go with the First Asset Canadian REIT ETF (TSX: RIT). It’s more diversified (37 holdings as opposed to 18 for XRE) and has a better long-term track record. The MER is 0.75 per cent. The monthly distribution is $0.0675 per unit. We’ll buy 150 units at $17.30 for an investment of $2,595.

I also want to add a Canadian equity fund and an international fund to the portfolio to replace the two equivalent mutual funds. Here are my choices.

BMO Low Volatility Canadian Equity ETF (TSX: ZLB). This ETF invests in a portfolio of large-cap Canadian stocks that have a low beta history, meaning they are less sensitive to broad market movements and, therefore, less risky. Top holdings include companies like Fairfax Financial, RioCan REIT, Emera, and Intact Financial. This ETF invests in a portfolio of large-cap Canadian stocks that have a low beta history, meaning they are less sensitive to broad market movements and, therefore, less risky. Distributions are paid quarterly. The MER is 0.39 per cent. We will buy 150 shares at $31.43 for a cost of $4,714.50.

BMO Low Volatility International Equity Hedged to Canadian Dollar ETF (TSX: ZLD). I like low-volatility funds for an RRSP for one very simple reason: they are designed to mitigate losses in bad markets. The worst enemy of your retirement plan is a serious setback, such as many people experienced in 2008. So, let’s stick with the same theme for international investing with another fund from BMO. It’s hedged to Canadian dollars, so the currency risk is removed. This fund has not been around long, but it shows a two-year average annual return of 9.2 per cent, which is very good in the context of global markets. It invests in units of ZLI, a companion low-volatility fund that is unhedged. Distributions are paid quarterly, and the MER is 0.45 per cent. We will buy 100 units at $24.04 for a total of $2,404.

That brings our total new investment to $15,529.50. We’ll take $269.86 from cash to make up the difference.

Finally, we will buy another 40 units of the Beutel Goodman American Equity Fund at $14.77 for a cost of $590.80. That will leave retained earnings of $53.49.

That leaves a cash balance (including retained income) of $1,447.46, which will keep in our EQ Bank account at 2.3 per cent.

Here is the revised portfolio. I’ll review it again in August.

RELATED:

Q&A With Gordon Pape: Will A Spousal RRSP Reduce My Tax Bill?

Do you have a money question you’d like to ask Gordon? Find out how to submit it here and then check out our Money section regularly to see if it was chosen for a response. Sorry, we cannot send personal answers.

'%3E %3Cg id='Group'%3E %3Cpath id='Vector_2' d='M12.4876 13.8996V13.4213H0.743091V15.2149H9.18805L9.22196 15.2685C9.19653 15.2272 3.24373 25.2836 0.74521 29.5469C0.420975 30.1015 0.0797856 30.7158 0.0797856 30.7158C0.0713089 30.7323 0.0585938 30.755 0.0585938 30.755H12.1401V28.9614H3.67181L3.6379 28.9078C3.37512 29.1222 12.4876 13.8996 12.4876 13.8996ZM36.1229 22.115C36.1229 26.4896 33.7537 29.18 31.1683 29.18C28.5829 29.18 26.1861 26.4896 26.1861 22.115C26.1861 17.7403 28.5553 15.0231 31.1683 15.0231C33.7812 15.0231 36.1229 17.7403 36.1229 22.115ZM22.0155 22.115C22.0155 26.4896 19.6462 29.18 17.0587 29.18C14.4712 29.18 12.0765 26.4896 12.0765 22.115C12.0765 17.7403 14.4458 15.0231 17.0587 15.0231C19.6717 15.0231 22.0155 17.7403 22.0155 22.115ZM38.223 22.0613C38.223 16.7095 35.0443 13.1492 31.1661 13.1492C27.288 13.1492 24.3402 16.4312 24.0987 21.4326C23.8592 16.4333 20.7842 13.1492 17.0587 13.1492C13.3332 13.1492 9.97427 16.7074 9.97427 22.0613C9.97427 27.4153 13.1785 31.0003 17.0587 31.0003C20.9389 31.0003 23.8592 27.7183 24.0987 22.6922C24.3402 27.7162 27.4406 31.0003 31.1661 31.0003C34.8917 31.0003 38.223 27.4421 38.223 22.0613ZM51.3747 30.755H53.5257L52.3178 13.4213H50.1668L45.797 27.3328L41.4273 13.4213H39.2763L38.0662 30.755H40.2172L41.0352 19.0247L44.7205 30.755H46.8714L50.5567 19.0247L51.3747 30.755ZM53.9453 30.755H62.3797V28.9614H56.0963V22.9293H60.964V21.1357H56.0963V15.2128H61.8859V13.4192H53.9453V30.7529V30.755ZM69.3624 18.2021C69.3624 20.1029 68.1333 21.1625 66.7367 21.1625H64.893V15.2128H66.7092C68.1333 15.2128 69.3624 16.3261 69.3624 18.2021ZM71.5134 18.1753C71.5134 15.2128 69.3348 13.4213 67.0164 13.4213H62.7993V30.755H64.893V22.9313H66.7092L71.5112 30.755H73.997L68.8601 22.4695C70.369 21.8717 71.5134 20.3502 71.5134 18.1773' fill='%23231F20'/%3E %3C/g%3E %3C/g%3E %3C/g%3E %3Cg id='Group_2'%3E %3Cpath id='Vector_3' d='M9.67285 8.56629V3.50513H12.6249V4.11535H10.5947V5.71719H12.2943V6.32742H10.5947V7.954H12.9046V8.56423H9.67285V8.56629Z' fill='%23231F20'/%3E %3Cpath id='Vector_4' d='M17.6819 8.6137H17.2581L15.1855 3.50513H16.1392L17.0822 5.86975C17.2178 6.20991 17.362 6.63872 17.4976 7.05103H17.5188C17.6544 6.64696 17.7879 6.2264 17.9341 5.86975L18.8666 3.50513H19.7482L17.6862 8.6137H17.6819Z' fill='%23231F20'/%3E %3Cpath id='Vector_5' d='M22.4072 8.56629V3.50513H25.3593V4.11535H23.3291V5.71719H25.0287V6.32742H23.3291V7.954H25.639V8.56423H22.4072V8.56629Z' fill='%23231F20'/%3E %3Cpath id='Vector_6' d='M31.6164 8.56629L29.9698 6.32123H29.2959V8.56629H28.374V3.50513H30.0948C30.9552 3.50513 31.805 4.01227 31.805 4.90906C31.805 5.54402 31.3896 5.97283 30.8725 6.16249L32.6654 8.56629H31.6185H31.6164ZM29.9592 4.10711H29.2959V5.71719H29.9592C30.436 5.71719 30.8704 5.43888 30.8704 4.90906C30.8704 4.37923 30.436 4.10711 29.9592 4.10711Z' fill='%23231F20'/%3E %3Cpath id='Vector_7' d='M37.5849 6.27382V8.56629H36.6737V6.28206L34.6943 3.50513H35.667L36.6503 4.90081C36.8156 5.13789 37.0021 5.38528 37.1378 5.59968H37.159C37.3031 5.39353 37.5001 5.11522 37.657 4.90081L38.6403 3.50513H39.5621L37.5828 6.27382H37.5849Z' fill='%23231F20'/%3E %3Cpath id='Vector_8' d='M44.3084 4.11535V8.56629H43.376V4.11535H41.7188V3.50513H45.9656V4.11535H44.3084Z' fill='%23231F20'/%3E %3Cpath id='Vector_9' d='M52.0484 8.56629V6.32948H49.499V8.56629H48.5771V3.50513H49.499V5.71926H52.0484V3.50513H52.9808V8.56629H52.0484Z' fill='%23231F20'/%3E %3Cpath id='Vector_10' d='M56.2129 8.56629V3.50513H57.1453V8.56629H56.2129Z' fill='%23231F20'/%3E %3Cpath id='Vector_11' d='M64.7402 8.64463L62.4091 6.17693C62.0467 5.79553 61.6208 5.31106 61.2796 4.91524L61.2584 4.92349C61.2796 5.3523 61.2902 5.7811 61.2902 6.13776V8.56629H60.3789V3.50513H61.0316L63.1868 5.82233C63.4878 6.14806 63.9222 6.63872 64.2337 7.00362L64.2549 6.99537C64.2337 6.62223 64.2231 6.17899 64.2231 5.83677V3.50513H65.1344V8.64669H64.7402V8.64463Z' fill='%23231F20'/%3E %3Cpath id='Vector_12' d='M70.9048 8.64416C69.4235 8.64416 68.0566 7.69172 68.0566 6.03421C68.0566 4.37671 69.4659 3.41602 70.8752 3.41602C71.5999 3.41602 72.17 3.57476 72.5324 3.78091L72.3883 4.42412C72.0471 4.21797 71.5491 4.05098 71.0002 4.05098C69.9639 4.05098 68.9912 4.77253 68.9912 6.04246C68.9912 7.31239 69.9448 8.01745 70.9599 8.01745C71.405 8.01745 71.7567 7.93911 71.975 7.7948V6.61352H70.8349V6.03421H72.8354V8.12877C72.3586 8.47718 71.7271 8.64416 70.9091 8.64416H70.9048Z' fill='%23231F20'/%3E %3C/g%3E %3Cpath id='Vector_13' d='M0.0839844 1.00212L73.997 1' stroke='%23231F20' stroke-width='1.25' stroke-miterlimit='10'/%3E %3Cpath id='Vector_14' d='M0.0839844 10.9116H73.997' stroke='%23231F20' stroke-width='1.25' stroke-miterlimit='10'/%3E %3Cpath id='Vector_15' d='M4.91016 4.15649L3.55812 4.13794L5.18777 5.7068L0 5.6532V6.5974L5.20049 6.651L3.61321 8.18068L4.96526 8.19718L7.0018 6.20157L4.91016 4.15649Z' fill='%23D71920'/%3E %3C/g%3E %3C/svg%3E)